Felix 2020 - Year Review

.jpg)

It would be remiss of us not to look back at how Covid-19 has re-shaped our ways of working, thinking and doing things. We stepped into new territories, but also recognised earlier lessons that needed to be re-learned.

As the historical year draws towards the end, we’d like to take a moment to reflect on the things that are important to us and the industries we work with.

Digitisation fast tracked

The very obvious manifestation of this is the unexpected remote work “experiment” that organisations around the globe have entered.

Like many others, Felix had to move to a fully remote setup overnight. Once restrictions eased, we evaluated the effectiveness of fully flexible work arrangements based on team spirits and productivity, and unanimously agreed that flexible work should be a permanent part of the company.

On a national scale, 75% of Australians now expect WFH to be the norm, which means:

“Companies will demand infrastructure that allows for the digitisation of businesses and remote working, more areas for team collaborations and a reduction in density levels, as well as an increase in hot-desking, supported by booking systems.”

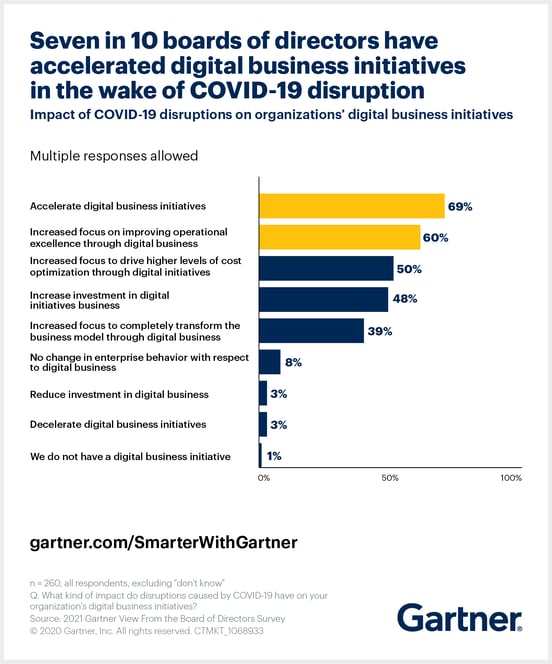

Plenty have pointed to the rise of cloud-based software and collaboration tools, or even an increase in digital transformation as a result of COVID-19. So for those who are still running on spreadsheets or paper-based systems, this can pose a great deal of challenges.

Source: Gartner

Unprecedented infrastructure boom

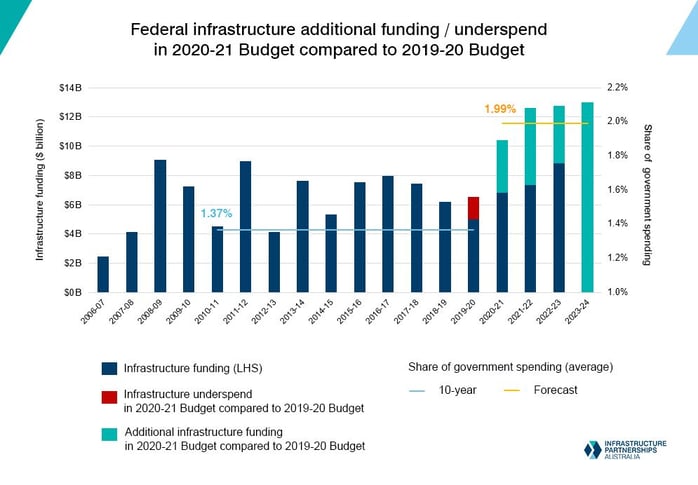

In this year’s Budget, the Government has lifted total infrastructure funding to $48.8 billion over the forward estimates.

That’s a $19.3 billion increase from the four-year spend set out in last year’s Budget, and represents the largest infrastructure funding allocation seen from a Federal Government in Australia’s modern history.

With the infrastructure-led economic recovery strategy, many have warned things need to change in order to make it work. The eye-opening report “The rise of megaprojects: counting the costs” by Grattan Institute outlines some key issues around cost estimates, decision making, risk allocation and more.

Some of these key themes around public procurement of major infrastructure projects were also covered in our webinar with Leah Singer - author of the report "Creating Value Through Procurement" commissioned by Infrastructure New Zealand.

This year, the Australian Constructors Association (ACA) has also launched the first-ever national Construction Industry Charter to spearhead reform, recognising that “construction industry profits collapsed between 2014 to 2018...and productivity growth rate since 1989/1990 for construction has been only half that of other sectors.”

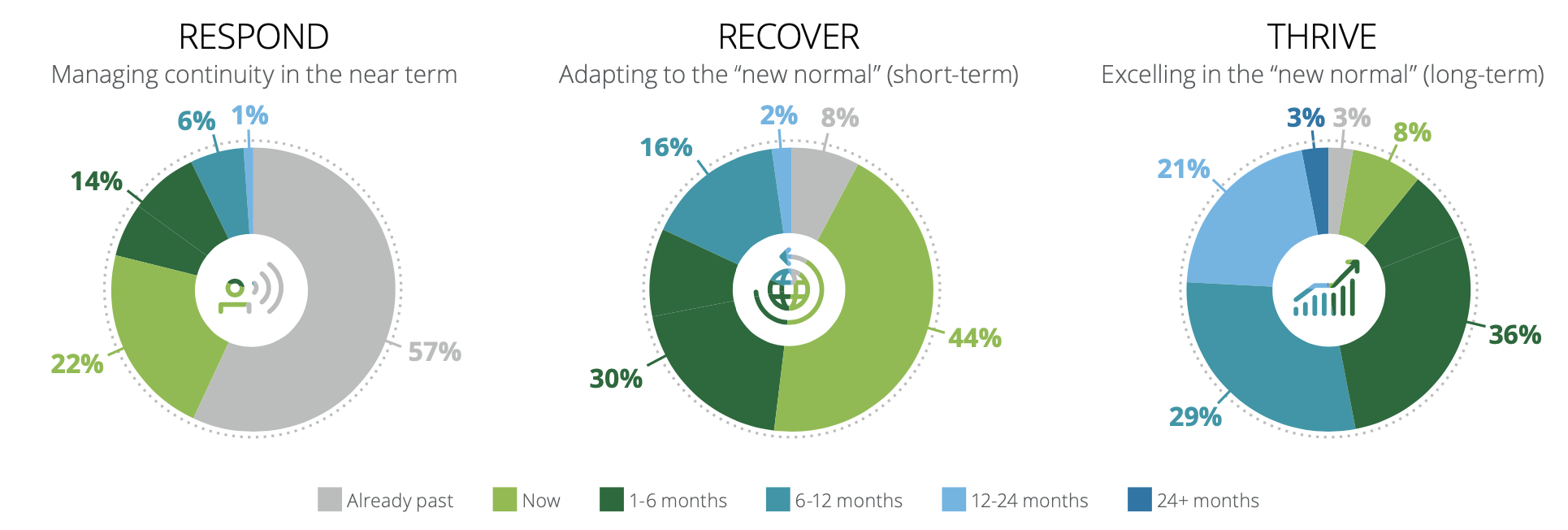

Risk management rushed to the fore

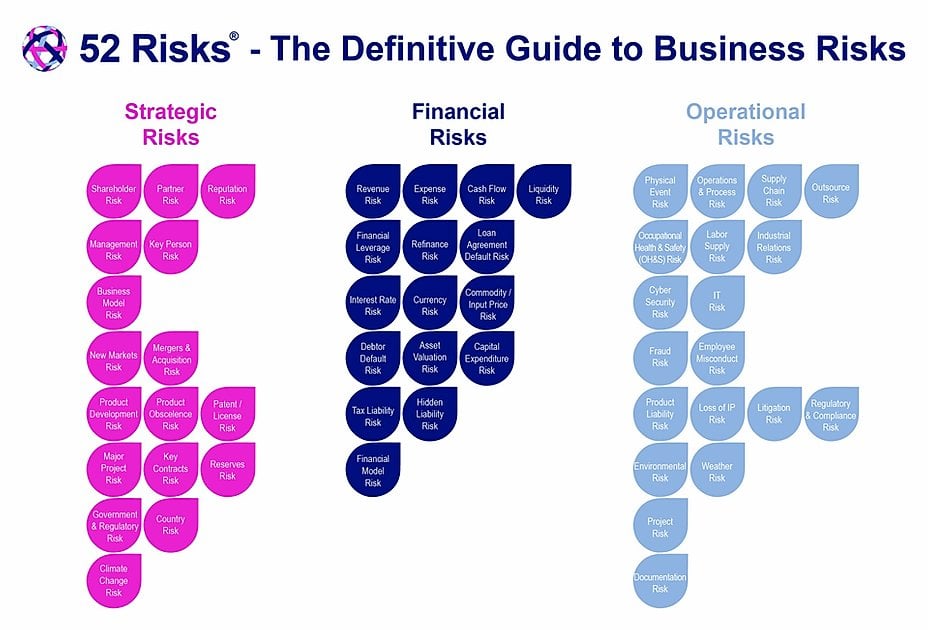

The “black swan” COVID-19 has exposed many types of risk. Borrowing the 52 Risks framework from Peter Deans (who did a risk mitigation webinar with us), we can broadly group them under 3 categories:

Source: 52 Risks

Pre-COVID, we had alarming stats such as “about 80% of Australia’s listed companies have never done scenario-planning" - which leads to this:

“Failing to invest in Supplier Risk and Management Technology was the No. 1 technology regret during COVID-19.” (Supply Chain Confidence Index, Procurious)

Business continuity planning and supply chain resilience suddenly became “cool.” We’ve also written on the importance of understanding your suppliers and segmenting them by risk - which are “old” lessons from previous disruption events.

Another way to look at risk is through a contract lens. With this year’s pandemic (and previously the bushfires and floods), there’s been a magnifying glass over force majeure, frustration and termination for convenience clauses in contracts.

However, in the 2020 World Commerce & Contracting Report on Most Negotiated Terms, Force Majeure is ranked 27th in Most Negotiated Terms, 17th in Most Important Terms and 10th in Most Claims.

Another noteworthy finding is that “priority is given to terms dealing with risk consequence, rather than risk prevention.” Perhaps this is because most organisations have been led on a reactive risk mitigation journey since the pandemic, and have only shifted to “Recover” mode recently.

Source: Deloitte

Responsible and sustainable procurement

Modern Slavery

In response to COVID-19, the deadline for the deadline for eligible entities with a consolidated annual revenue of $100 million or more to file a Modern Slavery Statement has been pushed back by 3 months.

Nonetheless, many organisations have already filed their report before the original deadline of 31 December 2020.

Source: Modern Slavery Register

Environmental, Social, and Corporate Governance

There is a wider theme of the “stakeholder economy,” particularly with COVID-19 exposing more vulnerable groups in society.

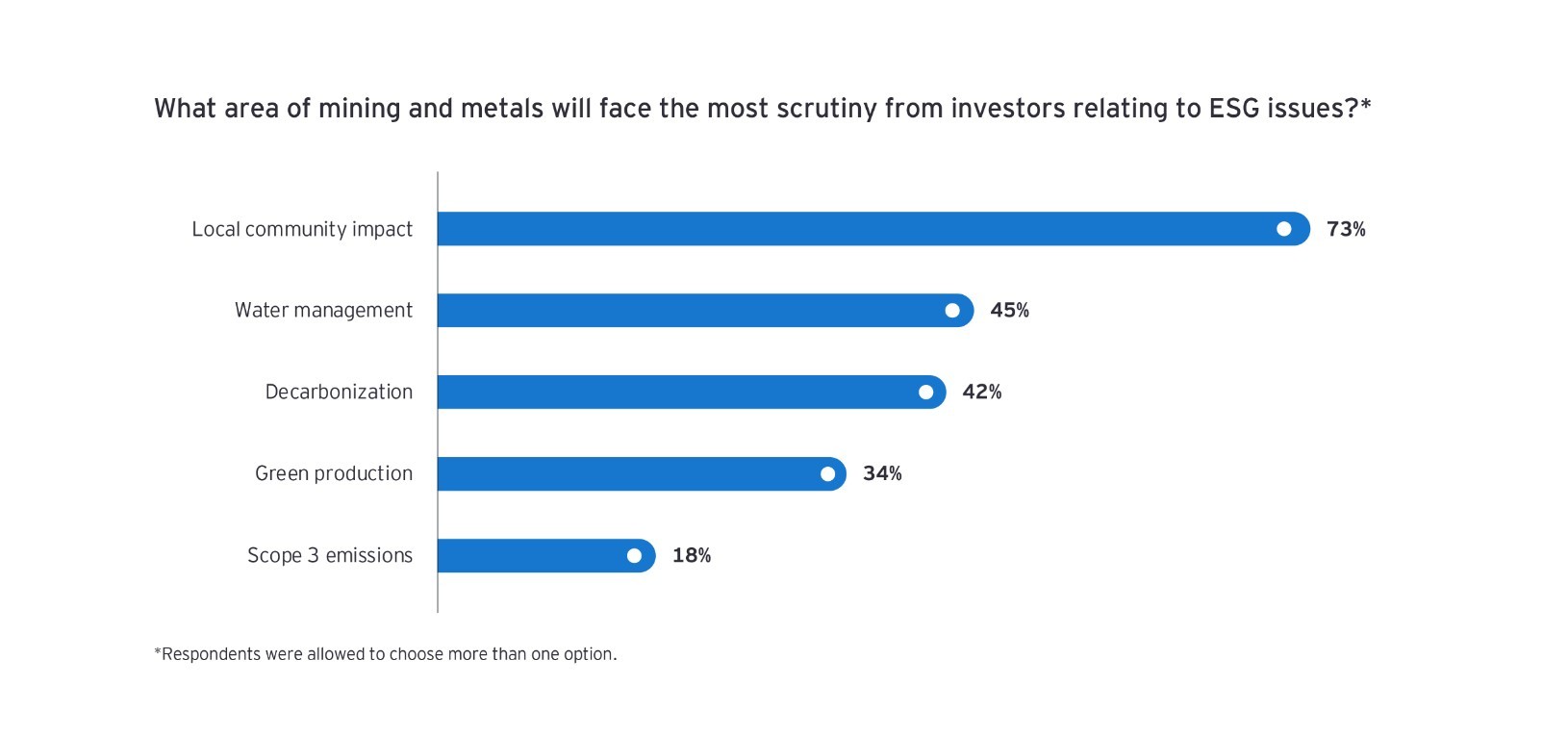

In the Mining & Resources sector for instance, license to operate remains the top concern according to the recent EY survey.

The latest public outcry over the sacred Juukan Gorge caves destruction serves as a stark reminder to consider the wider stakeholder groups.

Source: EY

We’ve previously reported that from July this year, the Indigenous procurement targets would be mandatory in high value contracts across 19 industries (instead of the current 8), with “Mining and Oil & gas services” among the newly added.

As a direct or indirect result of these socially responsible procurement policies, the Indigenous business sector has seen a 12.5% annual growth rate, making it one of the fastest growing in Australia.

The same could also happen for social enterprises if the call for a mandated 1% sustainable procurement target on all Government contracts comes through.

Circular infrastructure

The pandemic has challenged everyone to “rethink and redesign for resilience.” While the circular economy is not a foreign concept, circular infrastructure has just started to become more relevant.

Specifically, in February this year, the 2020 Infrastructure Priority List adds national waste and recycling management as one of 5 new national priority initiatives. So watch this space for more initiatives from the government down the track.

New developments inside Felix

A lot has happened within our own organisation over the last 12 months too.

We’ve merged brands and become one under the Felix roof. Our sister brand PlantMiner – where it all started for us – became Felix Vendor Marketplace this September.

What that means is our enterprise customers can now seamlessly tap the open marketplace during RFQs. Check out our previous announcement from the CEO for more.

Whilst adapting to the remote work environment, the Felix team has pushed through a bunch of new features and updates to our core platform, including the expanded Felix API, project grouping, sign-off workflow overhaul, endless security and infrastructure improvements. Before the end of the year, we’ll have expanded our internationalisation capabilities to sourcing.

I’m extremely proud of each and every one who has pulled their weight to make it happen at Felix.

Finally, on behalf of the organisation, I wish our clients, subscribers and readers a very Merry Christmas. Here’s to forging meaningful relationships in 2021.

Related Articles

Modern Slavery, ESG, reforms and why you should care (Part 2)

Modern slavery is part of the S in ESG, how do you treat people?

It's particularly relevant to the construction industry, which might surprise some of you, as it's considered a high-risk industry.

Why organisations need a standardised vendor prequalification framework

Low productivity and increasing tendering/procurement costs have traditionally been among factors driving downward pressures on margins, for both contractors and their supply chain. Moreover, legislative requirements around sustainable procurement are adding another kind of pressure.

How social procurement is much more than corporate social responsibility

Are you leveraging social enterprises in your tenders? Because your competitors are. There's a growing expectation for contractors to include social enterprises when bidding and delivering commercial and major government projects, yet navigating social procurement remains an afterthought for many.